Table of Content

Credit line may be reduced or additional extensions of credit limited if certain circumstances occur. Available on 1-4 family owner-occupied properties located in Wisconsin only. Vice versa, the slower you repay your loan, the higher your financing costs will be. How fast you repay your mortgage loan depends on the amount of your monthly rate and additional repayments you may make. In Germany, most banks offer the option of additional repayments between 5% and a maximum of 10% per year. When you want to buy a home in Germany, you’ll almost certainly need to take out a mortgage.

However, the amount you can borrow and your deposit depends on your residency status and financial circumstances. Our advanced technology compares mortgage options from over 400 German lender and our mortgage experts will explain each offer. Your personal mortgage expert will support you to review and understand all your options. To find you the optimal mortgage, we will use our unique Hypofriend Recommendation Engine. We will begin by asking you several key questions, which will help us determine which mortgage products could work best for you.

How to apply for a mortgage in Germany

The mortgage approval is a binding document which certifies that your lender will support you with the funding. Once you've selected your mortgage offer, we will provide you a document checklist that shows all the required document you need to submit. Together with our team of experienced brokers, you will understand the nuances of your situation and fine-tune your mortgage decision.

However, it is possible to take out a separate personal loan for this purpose. Furthermore, your monthly repayment should be calculated realistically, so you can easily cover it without having to restrict your accustomed standard of living. This German mortgage calculator is designed to help you determine the estimated amount you can get from over 750 mortgage lenders in Germany.

Join our 10000+ clients from all across Germany

Germany’s rental market can be very competitive, especially in major cities where most people are tenants. Initial tenancy periods in Germany can be as long as two years. Some tenancies are indefinite, meaning they’ll run until the landlord or tenant serves notice to break the agreement. Expats looking to buy a home in Germany can take out a mortgage with no restrictions.

If you live and work outside of Germany, you’ll usually only be able to borrow around 60% of the property’s value, meaning you’ll need a deposit of at least 40%. Germany’s property system encourages investment in the rented sector, with favorable tax incentives available for residents who purchase buy-to-let properties. There are several types of mortgages to choose from in Germany. Banks in Germany offering mortgages to expats include DKB and Santander.

Get matched with the best mortgages for your situation

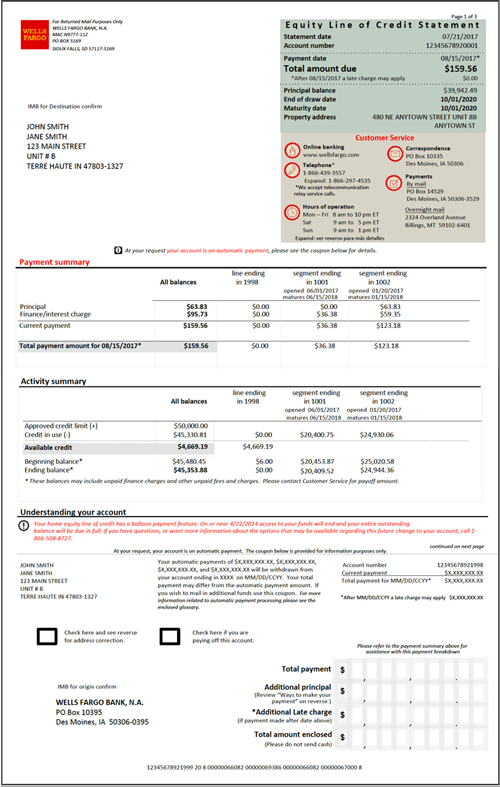

You should be able to access your home equity account normally within 3 business days after your closing. We'll review your credit application in accordance with our normal credit approval processes. Your home's equity can be calculated by subtracting any outstanding mortgage balance from the market value of the property. For example, if the appraised value of your home is $250,000 and the principal balance remaining on your mortgage is $150,000, then your home equity is $100,000. If you choose to rent, your options will depend on the area you choose.

Data from Statista shows that Germany was one of only three European countries to have more than a trillion Euros of outstanding mortgage balances in 2021. In your secure online account, you can easily upload your required personal, property and mortgage documents to get approved faster than traditional brokers. We'll calculate your maximum property budget based on your income, savings, residency status and the criteria of our 750+ partner banks. This depends on several factors, such as the amount of the mortgage and how much you want to pay back monthly. The rule of thumb is that the monthly mortgage payment should not exceed 40% of your net income.

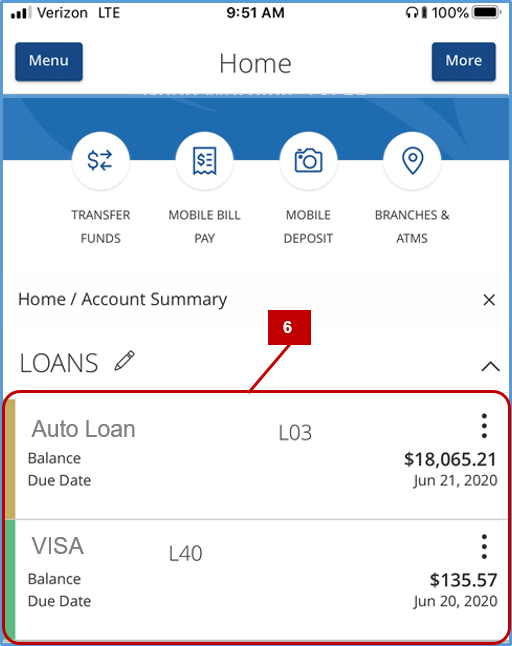

Visit any of our convenient locations or contact one of our loan officers to hear about our current home equity rates. Our lenders are here to work through the options with you, to find your perfect home equity match. Whether you want to build your first home, purchase a vehicle, or even expand your business; we will help you along the way with loans tailored to your specific needs. The Citizens Bank International Visa Credit Card gives you access to credit you can spend to make purchases online or anywhere Visa cards are accepted locally or internationally. A line of credit that gives you access to cash at your disposal.

This involves switching to a new mortgage with your current bank or a different provider. Interest on German mortgages for owner-occupied properties is not tax-deductible. However, if you rent out a property in Germany, expenses for generating rental income can be offset on your tax bill. In addition to the wider economic situation and your financial circumstances, rates will vary depending on how long you fix them for. For example, if you fix for five years at a rate of 2.5%, you might expect to pay 2.8% if you fix for 10 years, or 3.1% for 15 years. Non-EU citizens may find it more difficult to get approved without a big deposit unless they have a permanent residence permit.

If you wish to refinance before then, you’ll need to pay early repayment charges (Vorfaelligkeit-sentschaedigung). These charges can be very high, so it’s better to wait until the end of your term to switch deals. First, use a mortgage calculator to get an idea of how much you might be able to borrow when taking out a home loan. Once you’ve got this indication, you may want to take advice from an independent mortgage adviser. Independent advice can be useful if you’re new to the German mortgage system, are self-employed, or have unusual residency status. Once the mortgage lender has received the required payment order documents, they will pay out the loan.

Combining this lender know-how with given information and projected information , we evaluate a range of scenarios and outcomes to see how you will fare under different conditions. We discuss the outcomes and logic of the recommendations with you. You are different from the average customer, sometimes a little and sometimes a lot. We work hard to show you up-to-date product terms, however, this information does not originate from us and thus, we do not guarantee its accuracy. Before submitting an application, always verify all terms and conditions with the offering institution.

The more equity or savings you bring in, the lower your loan-to-value ratio LTV and hence the interest rate at which the bank grants you your mortgage. Typically, banks lower the interest rate gradually in 5% steps of the LTV. In other words, a higher down payment means a lower LTV and a lower interest rate, and vice versa, a lower down payment means a higher interest rate due to a higher LTV. To optimize the recommendation engine, we review daily the mortgage products and conditions of over 750 lenders.

Fixed interest rateThe longer you fix the interest rate, the more security you have in planning your mortgage loan. However, you also have to accept higher costs, because the longer the fixed interest rate, the higher the interest rate that the bank will call. With a short fixed interest rate period, on the other hand, you benefit from a lower interest rate. But you take a risk as a higher loan balance remains at the end of the fixed interest rate and you may have to take out significantly higher refinancing for it.

No comments:

Post a Comment